Introduction

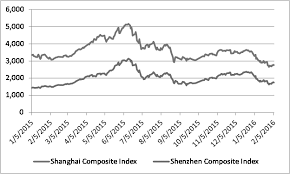

Rapid price increases were experience by the Shanghai Stock Exchange (SSE) and the Shenzhen Stock Exchange (SZSE) which are China’s two main stock markets in mid- 2014 to mid- 2015. However, a 32% and 40% fall in the composite indices of Shanghai and Shenzhen were experienced between June 12 and July 7, 2015. After the interventions of the Chinese government to halt the turbulence by using measures like stock purchases the stock prices stabilized for a brief period of time but in mid- August 2015 and in early 2016 there were sharp declines in the prices of the stocks. Various concerns over the health of the health of the Chinese economy and the resistance shown by the government to implement free market reforms were debated because of such volatility in the stock market and the government’s interventionists policies to regulate them. This volatility in the stock market did not just affect the Chinese stock market, but other indices were also greatly affected.

Source: (“China’s Recent Stock Market Volatility: What Are the Implications? –

Federation of American Scientists”, 2016)

Background and History

Established in 1990 as a part of the Chinese government’s effort to move towards domestic market capitalization, the SSE is world’s third largest stock exchange and SZSE is world’s fifth-largest stock exchanges which is based on domestic market capitalization. The ownership of Chinese equities by foreigners is relatively small and is extremely regulated, as a result only domestic Chinese firms are listed on the SSE and SZSE. As per the record of U.S. Department of the Treasury, the holdings of Chinese stock by the United States totaled to $98 billion at year end 2013, which was approximately 2% of China’s market capitalization and 1.6% of total U.S. global stock holdings.

The Chinese stock indices have experienced periods where high volatility was observed in the past which was similar to the v experienced in 2015-16. In the period of October 2006 to October 2007, the Shanghai Composite Index rose from 1,838 points to 5,955 which was a historical high, a 224% increase in the market index. But in early October of 2008, the index plunged back to the 1,800 mark. This decline was partially because of the global financial crisis

but many market analysts say that this correction of the bubble was driven primarily because of the rise in stock prices which was driven by speculation rather than the basic market fundamentals. A parallel of the same can be drawn to the turbulence in 2016-16. A rise of 108% and 177% was seen in the indices of Shanghai and Shenzhen in the period from June 2014 to June 2015. Chief economist at the International Monetary Fund, Olivier Blanchard said in July 2015 that this was “obviously a stock market bubble.” A decline of 43% and 44% respectively was seen in the SSE and SZSE from June 15 to August 25, 2015. Both the indices stabilized afterwards and then in the period between August 2015 to December 2015 the indices rose by 19.4% and 32.0%, respectively.

Causes of the Bubble

As per the report of Brookings Institution, the stock markets of China were heavily affected by the speculative investments made by marketers in Western countries. The Chinese markets focus on short term movements in stock prices because of the relatively less influence of the Chinese markets in comparison to their Western counterparts. There is a clear dominance of the retail investors in the Chinese stock exchanges who accounts for an estimated 90% of all market trades in the Chinese-based firms. According to a report, there were more than 30 million new trading accounts which were added in the first five months of 2015. It was seen that most of these individuals predicted that the prices of the stocks would continue to rise and bought these stocks on margin that is by using borrowed money. According to one of the estimates, approximately one-fifth of all money in the Chinese stock exchanges was financed by margin financing.

Response of the Chinese Government

There were numerous steps taken by the Chinese government to halt the slide in stock values which included forced cuts in the transactions costs and easing of the rules on margin trading. These steps were taken in order to guard against a potential wave of defaults. The Chinese government feared that the sudden slump in prices may lead to panic selling. In order to mitigate its impact, they got state owned firms and limited the sale of such stocks. They were able to do so by controlling the shareholders or the company executives. The government

threatened to arrest the individuals who even would try to manipulate the market in any possible way. This resulted on some analysts to believe that the governments intervention may indicate their unwillingness to liberalize the market system. Various debates started over this interventionist role of the Chinese government. Analysts questions whether these aggressive measures taken by the government were in lieu of the government’s claim to allow the market to play a decisive role on the correct allocation of the resources and the direction of the economy. Analysts believed that in many of the developed economies, the role of the stock market is to reallocate the resources to the businesses who would be able to better utilize these resources but in the case of China, this was on the discretion of the government. They further stated that such interventionist roles might prevent the government from political embarrassment of a stock market meltdown but through this process the government has made the task of modernizing the Chinese economy more difficult.

A new stock market circuit breaker was implemented by the China Securities Regulatory Commission (CSRC) to halt trading. The intent of the move was to limit sharp swings in the exchanges by imposing a “cooling off” period. The circuit breaker mechanism was triggered on January 4 and January 7 through which trading in the SSE and SZSC was halted. This move was suspended by the CSRC because it hadn’t worked as intended and if continued would lead to a magnet effect on certain investors. In succession to this the CSRC announced new limits in stock trades.

Implications

There were signs of concerns shown by some of the observers who feared that this continued fall in stock prices could have a disastrous impact on the Chinese economy which would lead to the consumer demand to lower itself because of the losses occurs by the retail investors. However, the Chinese stock market is small contributor to the economic activity in comparison to what other stock exchanges contribute in many countries. The direct exposure of the Chinese people to the market is only 5-10% as compared to 54% of that of the United States. These statistics indicate that in the situation of a huge slump in the stock market, the households and the domestic economy will have little impact but analysts are concerned with the implications of the Chinese government’s intervention in economic decision-making frontier in

the coming years.

Conclusion

If these policy decisions are to serve as a basis for future policy decisions it might be a situation of alarm and the fundamental idea of China to let the market allocate the resources. Such strategies of the Chinese government may lead to a hinderance in the efforts of the U.S, on issues such as the bilateral investment and market access. Questions over the overstated health of

the Chinese economy that some of the Chinese statistics provided coupled with the skepticism on the ability and willingness of the Chinese government to meet the commitments of the free market reforms.

References

China’s Recent Stock Market Volatility: What Are the Implications? – Federation of American Scientists. (2016, February 11). Retrieved from

https://fas.org/sgp/crs/row/IN10325.pdf

Yan, C. (2019). China’s stock market crash…in 2 minutes. Retrieved from

https://money.cnn.com/2015/07/09/investing/china-crash-in-two-minutes/

Kaletsky, A. (2019). China is Not Collapsing | by Anatole Kaletsky. Retrieved from https://www.project-syndicate.org/commentary/why-china-is-not-collapsing-by-anatole-kaletsky- 2015-10?barrier=accesspaylog